Powered with their own AI, Hims & Hers, Ticker: HIMS, is changing the Digital Healthcare Market by disrupting the ~$4 trillion healthcare industry creating a telehealth offering that brings quality, access, and affordability. Can Hims & Hers reach a market capitalization of 50 to 100 billion in the next 10 to 20 years?

updated: 7th of April 2025

Founder and CEO Andrew Dudum is the largest shareholder and visionary of the company and the entire TeleHealth industry. Andrew Dudum has taken on America's broken healthcare system by making his solutions affordable to everyone, regardless of insurance status, and creating a recognizable brand with HIMS. Dudum and his team are focusing on investing in growth and innovation and leveraging economies of scale. The customer experience makes HIMS the company it is today: successful. The people behind Dudum are also very experienced. Kåre Schultz was added to the Board of Directors. Schultz worked at Novo Nordisk for almost three decades, where he held various leadership positions.

$50-100 billion healthcare giant

Dudums’ goal is to make HIMS a $50-100 billion healthcare giant. We currently have a valuation of $6 billion. Here he says that a market capitalization of 50 to 100 billion can be achieved in the next 10 to 20 years!

Source: https://www.thefounderhour.com/episodes/andrew-dudum-hims-hers.

The rule of 40

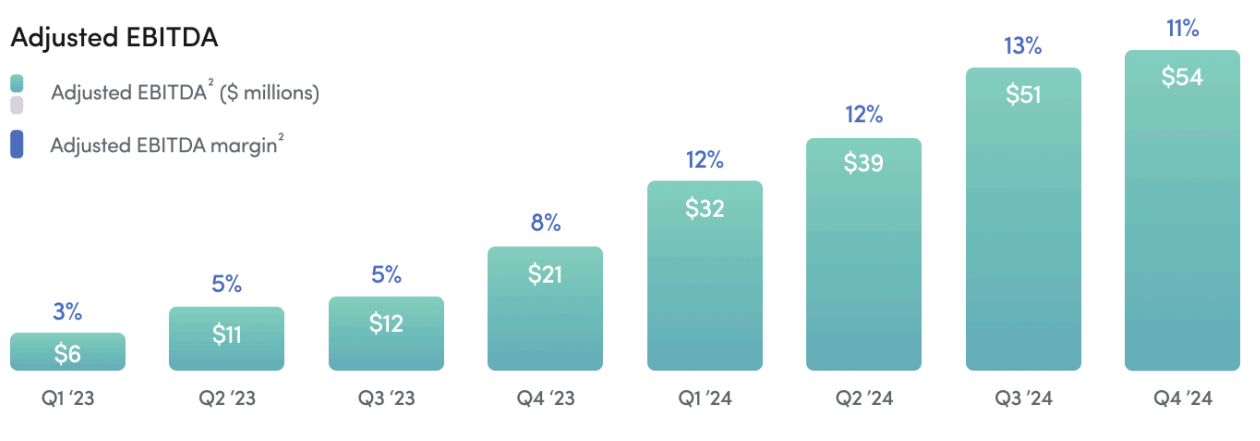

The rule of 40 for (growth-)stocks states: the growth rate (in%) and profit margin (in%) added together must be greater than 40%. Only then will the share, at first glance, be a fast-growing and highly profitable company. For HIMS the growth rate is 95% and the profit margin is 11% = makes 106. Accordingly, with 106 HIMS is well above the threshold of 40, indicating a very capital efficient growth.

HIMS detects health problems early

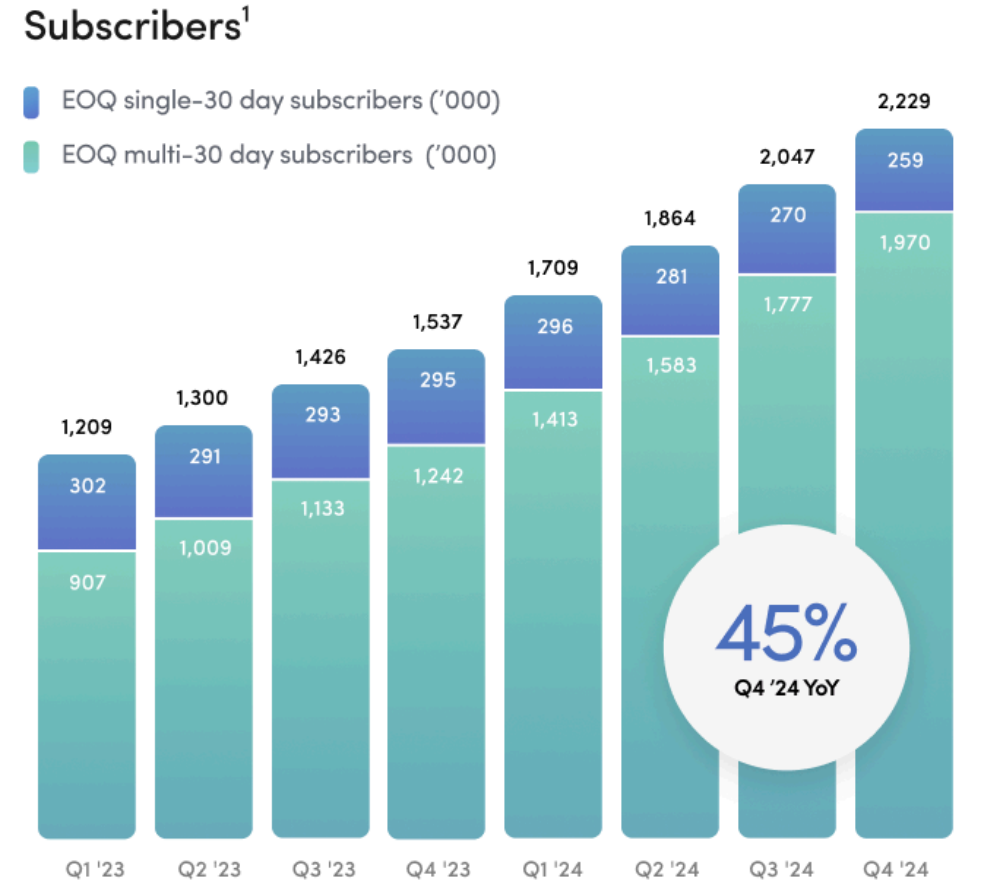

HIMS business model focuses on the future behavior of people: HIMS detects health problems early and focuses on the needs of customers. HIMS weight loss segment was the fastest ever to reach $100 million in annual sales and is expected to continue to gain momentum. New segments typically take 18-24 months to reach 100,000 subscribers. The weight loss reached this milestone in just 7 months. This non-GLP-1 weight loss solution from HIMS is performing incredibly well and overall Subscribers are growing strong: +45% in Q4’24.

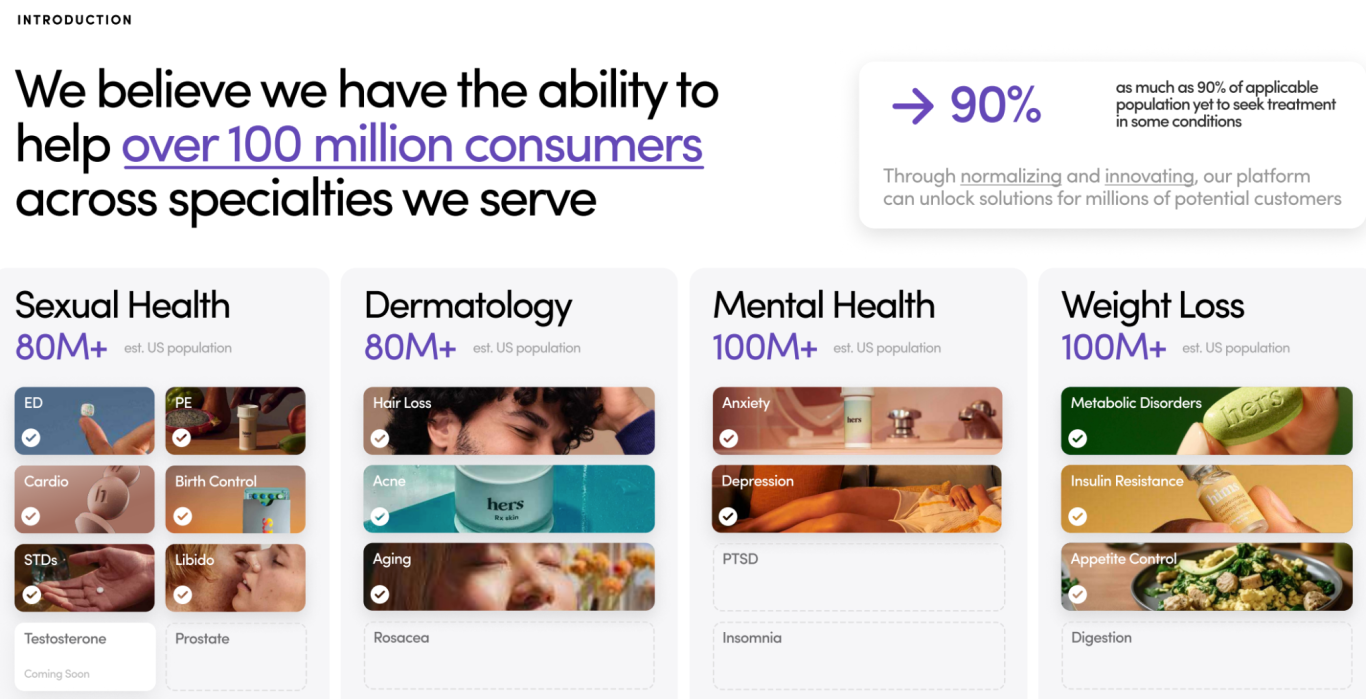

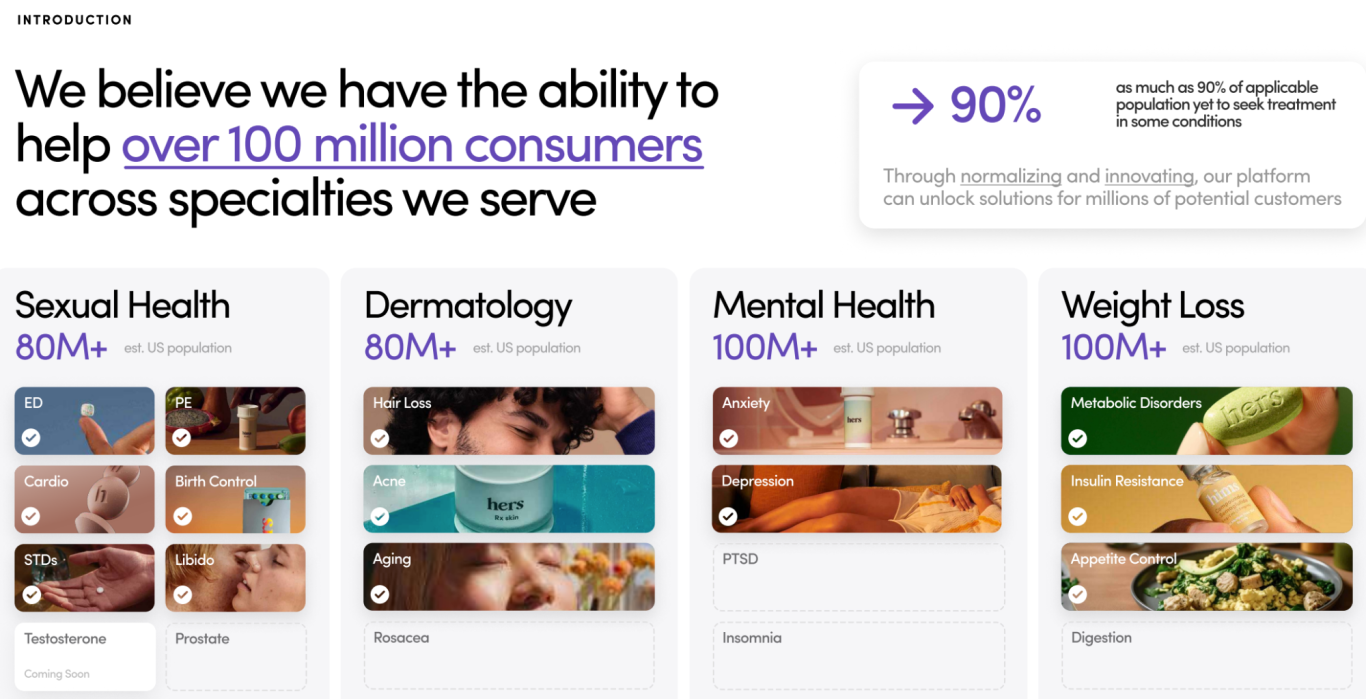

TAM is virtually endless

HIMS has built a strong moat through its brand awareness. The TAM is virtually endless. Sexual Health, Dermatology, Mental Health, Weight Loss and much more is about to come.

HIMS moat

I want to talk more about HIMS moat because it is often misunderstood.

Brand Awareness: What makes HIMS special is their value proposition. If a company's value proposition is better than that of its competitors, its moat may be smaller. Investors who focus on moats rather than value propositions are putting the cart before the horse. The value proposition creates the moat, not the other way around. HIMS' value proposition is that it is the lowest cost provider, offers 24/7 service and creates custom services, and is convenient/easy to use for customers. All of these aspects together ensure that users keep coming back to the platform. Over time, Hims' value proposition will create a noticeable moat. Now, if another company wants to compete with HIMS, it has to exceed Hims' value proposition, not cross its moat.

Personalized healthcare services: “One-size solutions” often don’t work because every body is unique. HIMS ability to personalize solutions increases the effectiveness of products to prevent side effects and increase effectiveness.

All-in-one meditation: “multi condition offerings” have the advantage that the treatment for many illnesses/symptoms is contained in one tablet/medication. This means that customers do not have to take many pills/medications one after the other.

MedMatch AI: MedMatch is a machine learning AI developed by HIMS. The AI tool helps HIMS determine the optimal treatment for a specific person: from dosage strength to form factor, among other things The model is initially based on the input of specific consumer data and previous experiences such as health history, symptoms, treatments, etc. Using this personalized data, HIMS creates a digital medical record, which is first reviewed by licensed healthcare providers (doctors) and then creates a perfectly tailored treatment plan . Once the data is reviewed, MedMatch helps healthcare providers create a customized prescription using data-driven recommendations.

Crossselling: MedMatch can not only create an individual product for customers for their health problem, but also identify additional problem areas by using millions of anonymized data points from millions of customers. Various illnesses or health needs can be treated.

„HIMS is only a GLP-1 company"

Let's discuss the „HIMS is only GLP-1 argument": Everyone is going crazy about HIMS losing its Compounded Semaglutid segment. There is ONE THING everyone forgot. HIMS has a non-GLP-1 weight loss solutions. HIMS weight loss segment was the fastest ever to reach $100 million in annual sales and is expected to continue to gain momentum. It typically takes 18 to 24 months for new segments to reach 100,000 subscribers. The weight loss reached this milestone in just 7 months. This non-GLP-1 weight loss solution from HIMS works incredibly well.

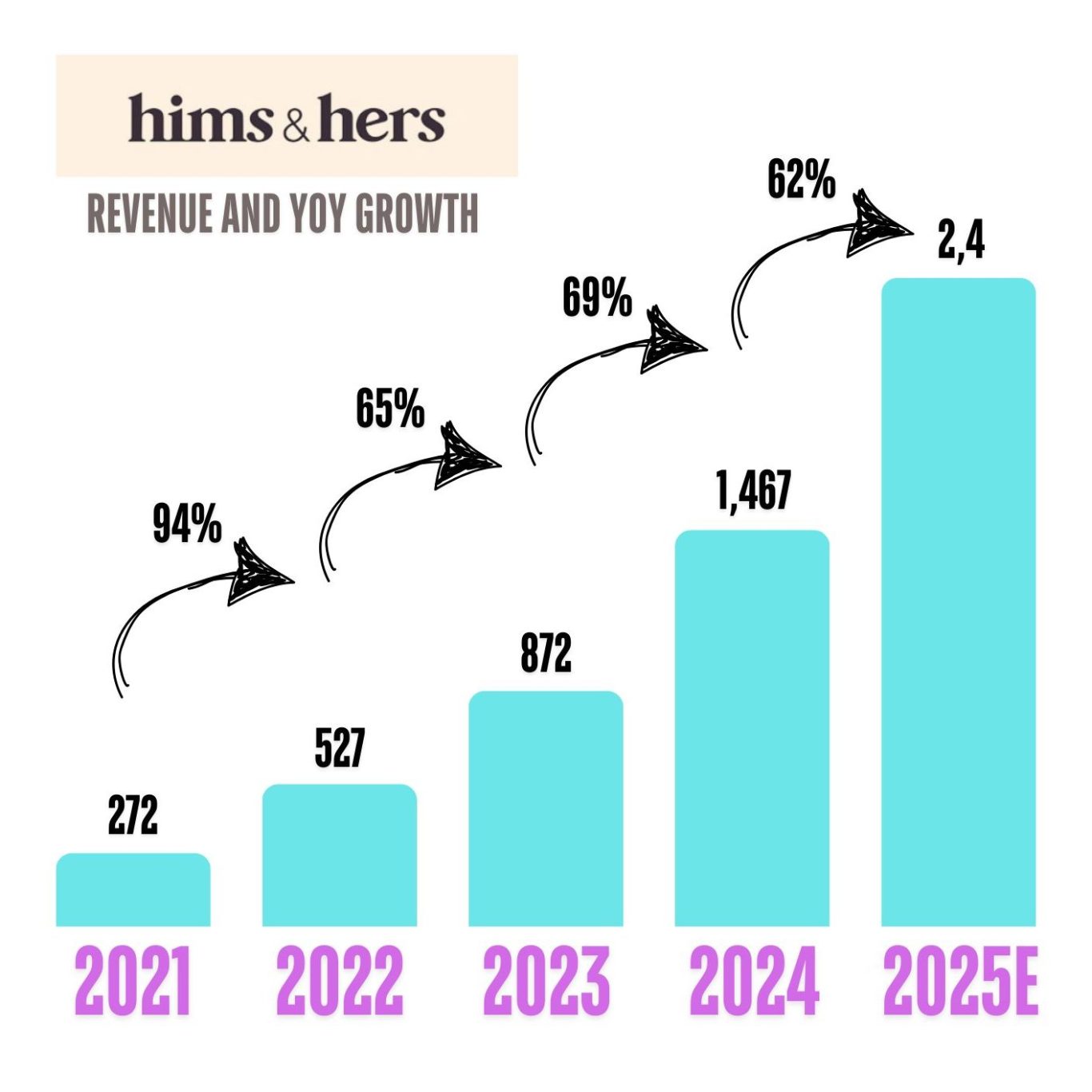

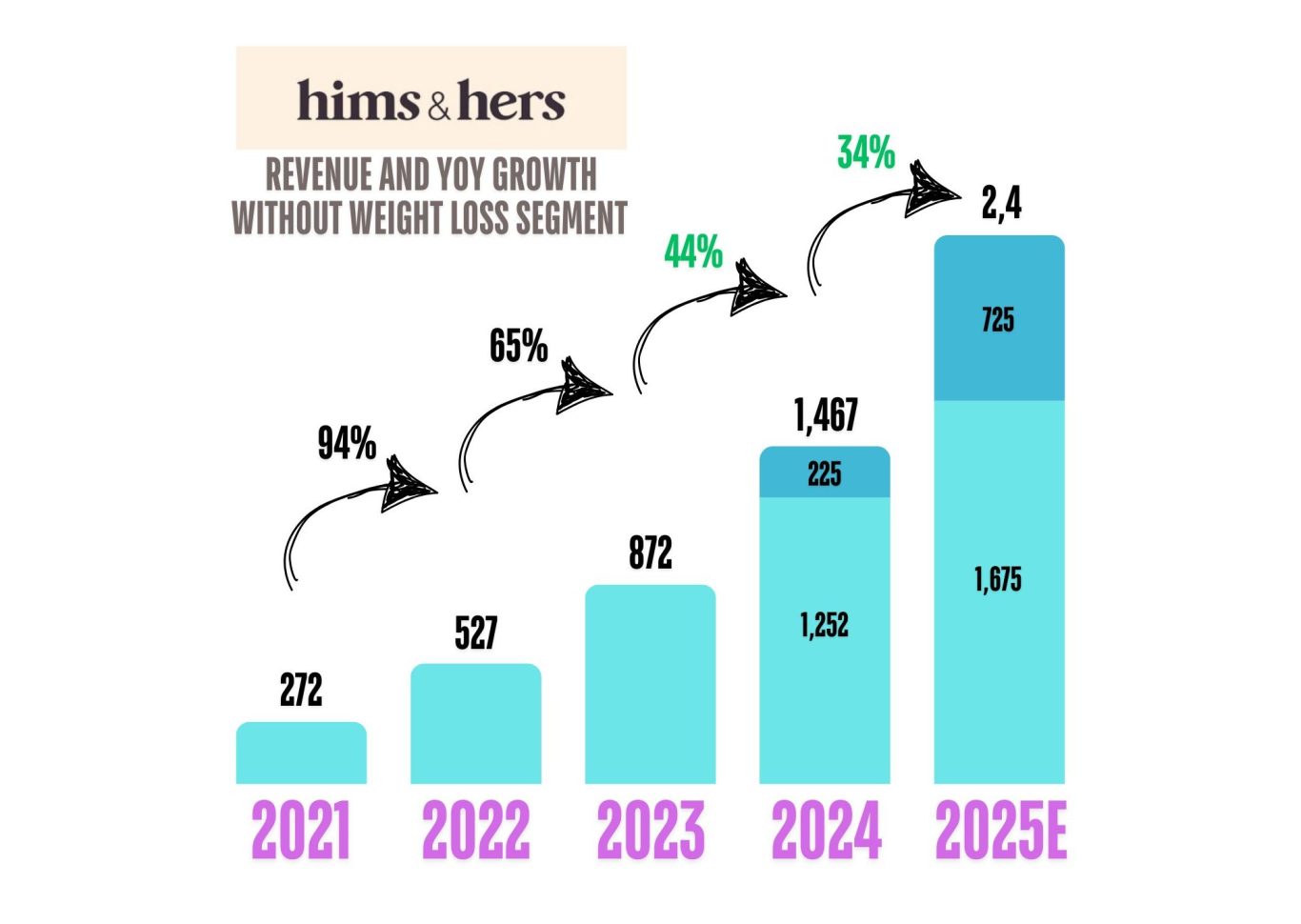

I have created two simple visualizations for you to illustrate this years stock fall. For the FY 2024 HIMS made $1.5 billion in revenue, which implies a growth rate of +70% YoY. Outlook for FY 2025: $2.4 billion in revenue, which implies a growth rate of +62% YoY. These figures are extremely bullish to me. But Mr. Market didn't eat HIMS lunch because Market expects much smaller growth rates due to the GLP-1 ban and a decline in sales as a result of that. Let's take a view on the Weight Loss Segment.

In FY 2024 HIMS generated sales of 1.5 billion, only $225 million came from the Weight Loss Segment. Of I calculate the Weight Loss sales from FY 2024 out, we get a growth rate of 44%. Let's do the same for FY 2025. HIMS expects $2.4 billion in revenue, $725 million will come from the Weight Loss loss segment. If I now take the Weight Loss segment sales out of FY 2025, we get a growth rate of 34%.

Conclusion: even without GLP-1 and the overall Weight Loss Segment which in addition to GLP-1, also combines oral medications, HIMS is growing at great figures.

HIMS bought TrybeLabs

There is literally no need to panic because HIMS lately bought TrybeLabs, a facility for at-home lab testing to access a breadth of data and biomarkers.

This acquisition will unlock a new level of personalized healthcare and deliver offerings across nutrition, lifestyle, supplements, medication and hormone levels. These Biomarkers include: cardiac risk, stress, cholesterol, liver function, thyroid function, and prostate health.

Looking at the very top level of the acquisition, HIMS just purchased a facility for at-home lab testing to access a breadth of data and biomarkers. On the surface, however, HIMS opens up an opportunity for a market comparable to GLP-1 & NVO.

TrybeLabs is revolutionizing personal health through accessible lab testing. As healthcare innovators and tech experts, the company recognized the need for seamless health monitoring from home. At TrybeLabs you simply order your at-home kit, collect the sample and mail it back to the CLIA and Joint Commission approved lab. A team of scientists will handle the rest.

The device is approved by the FDA. TrybeLabs delivers easy to understand results that provide health insights, score tracking over time and peer comparisons right to the phone on the HIPAA compliant portal.

The real value is that this acquisition will unlock an opportunity for a market by delivering AI-enabled diagnostic tests that are not only smarter but also highly personalized. The Blood Test Opportunity is an area where GH and GRAL are dominant and unlocking millions of Dollars already: Cancer Blood Tests. There are approximately 148.6 million people over the age of 40 in the U.S. If 75% of them undergo an annual physical and we assume a conservative cancer screening cost of $999, this represents a potential $110 billion market opportunity in the U.S. alone. Additionally, with 40% of men and women expected to be diagnosed with cancer at some point in their lives, the total addressable market (TAM) for cancer blood tests is enormous. I personally believe that HIMS aims to cover cancer blood tests in the longterm, too. It reminds me of what HIMS did with it's Compounded Semaglutid to rival NVO and LLY. TybeLabs is unlocking an amazing opportunity in the flield of blood testing. It just has begun.

MedMatch AI

Also AI is revolutionizing HIMS by enhancing patient care, data analysis, and operational efficiency. End of 2023 Andrew Dudum and his Team invented MedMatch AI, the Next Generation of Intelligent Diagnostic Services.

What's are the advantages?

1. Enhanced Personalization

- MedMatch analyzes millions of anonymized data points to recommend treatments tailored to an individual's unique needs. This improves patient outcomes by ensuring the most effective and appropriate care options.

- Customized Patient Care: Providers can access real-time insights, making it easier to address specific patient concerns, from mental health to weight loss, and more.

2. Efficiency for Providers.

- Streamlined Diagnosis: MedMatch reduces the time required for healthcare providers to determine the best course of action, enhancing the overall efficiency of telehealth consultations.

- Scalable Healthcare: Higher volume of patients.

3. Growth and Differentiation.

- Market Leadership: MedMatch positions Hims & Hers as an innovator in the telehealth space, differentiating the company from competitors.

- Customer Retention: Personalization means likely to see higher customer satisfaction and loyalty.

- Expanded Services: MedMatch supports the company's growth by allowing expansion into areas like mental health and weight loss, aligning with broader consumer health trends.

4. Data-Driven Learning

- MedMatch becomes smarter over time by learning from patient interactions, enabling ongoing improvements in treatment recommendations.

- Anonymized Insights: Big data ensures privacy / healthcare outcomes through advanced analytics.

5. Scalability for Various Conditions

- Initially launched for mental health services, MedMatch's potential to adapt to diverse health concerns like weight loss, sexual health, or chronic disease management means its applications are wide-ranging.

In essence, MedMatch benefits both users and providers by creating a more efficient, personalized, and accessible healthcare experience. For HIMS, it strengthens their value proposition, enhances their growth strategy, and positions HIMS as a leader in telehealth. HIMS will be able to create Intelligent Diagnostics by their AI coaches which will develop into AI android doctors. With over 15+ million estimated subscribers by 2030 and an operating system to make that data accessible HIMS will make near real-time and data-driven decisions to deliver personalized patient care.

In parallel, HIMS Lab Facilities will be able to facilitate the discovery, development and delivery of optimal therapeutics. Recent acquisitions set this path.

Andrew Dudum, CEO of HIMS has reopened the search to find a true visionary and AI & data enthusiast to join HIMS in transforming healthcare for millions of Americans. Why this Position is a pivotal role for the future growth of $HIMS:

HIMS is powering thousands of provider-patient interactions every day through their technology stack, which includes EMR and MedMatch. Deep value lies in their Data-Empire of over 2+ million subscribers with thousands more joining daily. What could this mean for the future?

AI in Healthcare Market was valued at USD 14.33 billion in 2023, and is expected to reach USD 153.61 billion by 2029, rising at a CAGR of 48.49%.

$HIMS positions itself in this market through the use of data and AI. With over 15+ million estimated subscribers by 2030 HIMS data engine gets more meaningful insights. The New CTO will expand MedMatch by building an infrastructure to leverage deeper AI.

The longterm goal is that on the one hand AI coaches can help optimize subscribers health, on the other hand these AI coaches will enable HIMS to install an empire of data and make a diagnosis before you even know you're sick. These AI coaches will develop into AI doctors.

The foundation of this future development is the acquisition of TrybeLabs. I already explained the value of that acquisition earlier above.

HIMS biggest threat?

Whats the HIMS biggest threat? A main risk I identified: Is AMZN a threat to HIMS? AMZN is trying to establish itself in the digital HealthCare Market since 6 years all they did is burning more than $6B . And NOW they are competing with "AmazonOneMedical" against HIMS:

BUT let's start in the year 2018. On June 28, 2018 AMZN announced the Acquisition of PillPack to "help people throughout the U.S. who can benefit from a better pharmacy experience“.

Source: https://www.cnbc.com/2018/06/28/amazon-to-acquire-online-pharmacy-pillpack.html.

The goal was to establish themselves as a cost-effective online pharmacy ... which failed.

On March 06, 2019 Amazon intended to disrupt the complete HealthCare Market by joining forces with Berkshire Hathaway and JPMorgan Chase. Together they created Haven.

Source: https://www.nytimes.com/2018/01/30/technology/amazon-berkshire-hathaway-jpmorgan-health-care.html

Haven, the joint venture formed by three of America's most powerful companies to lower costs and improve outcomes in health care, is disbanding after three years ... this project failed once again.

In 2019 AMZN Installed AmazonCare to roll out its telehealth Service nationwide. In 2022 AMZN did shut down "AmazonCare" and ... failed again.

Source: https://www.cnbc.com/2022/08/24/amazon-is-shutting-down-amazon-care-telehealth-service.html

The same year in 2022 AMZN acquired One Medical for $3.9B. Amazons' focus primarly was on the 15 years old Patient Data and on the approximately 250 medical practices that were in One Medical's network.

Also in 2022 AMZN re-branded AmazonCare with their new brand "AmazonClinic" to roll out again telehealth Services nationwide. This caused a 10% decline in HIMS stock in August, 2023.

And NOW they are re-branding AmazonClinic into „AmazonOneMedical“.

Source: https://www.fiercehealthcare.com/digital-health/amazon-one-medical-rolls-out-telehealth-treatment-services-competition-ro-hims-hers; https://health.amazon.com/prime?ref_=nav_cs_all_health_ingress_onem_h.

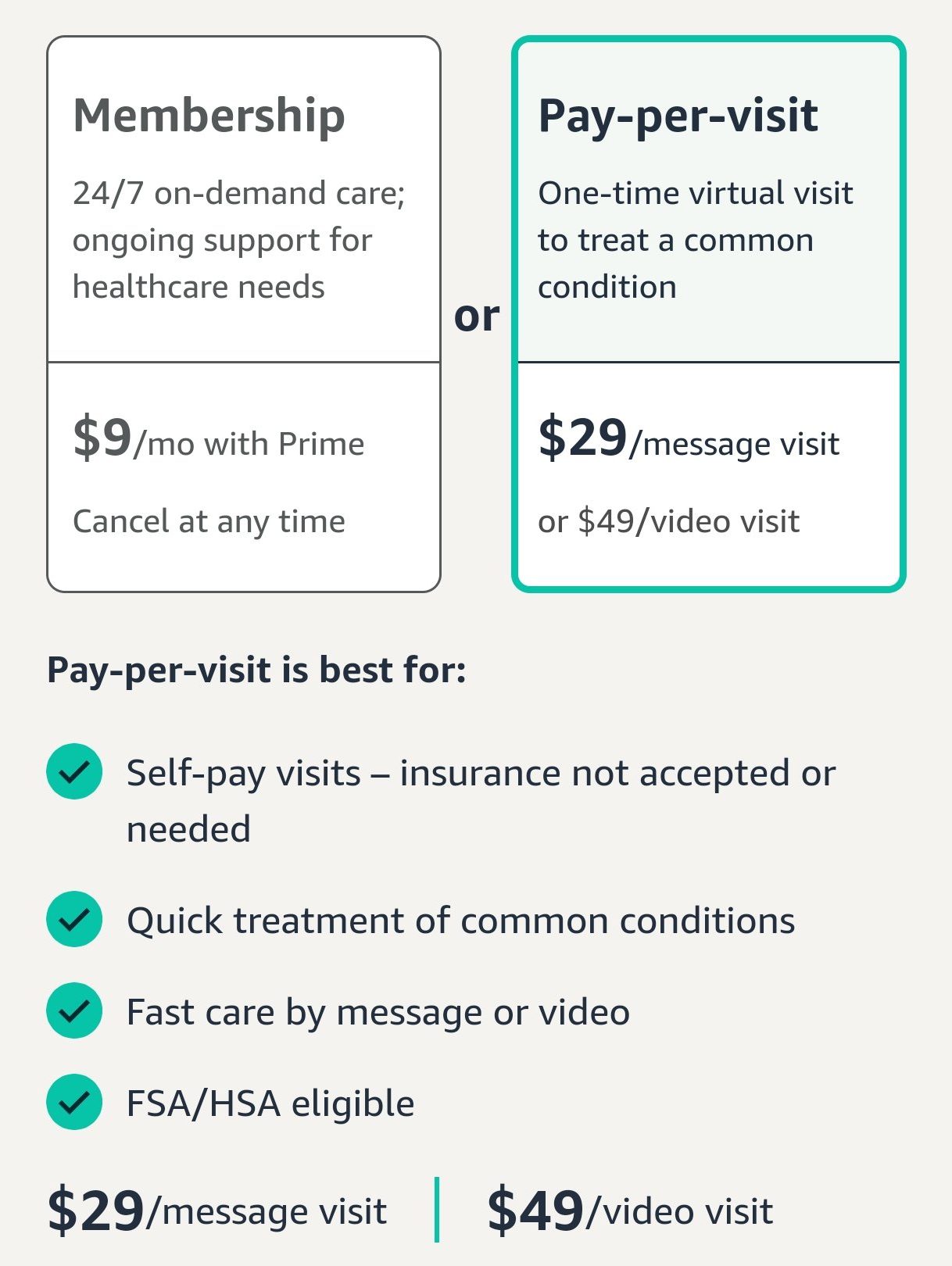

Let's dive into this "direct" competition which caused a 30% decline in HIMS Stock. Now Amazon tries to do the same thing as HIMS! But how exactly is it similar to HIMS? Let's take the example of hairloss. On Amazon, this is marketed at $16 per month. However, this offer can be described as "misleading" because the real costs also include either a text consultation for $29 or a video consultation for $49. The OneMedical membership costs $200 a year or $99 with Prime BUT you also have to pay for Prime membership.

HIMS offers its products at similar prices, but Amazon will not be able to compete with HIMS through a price war. It's simply too late for that.

Conclusion

HIMS makes over a billion in sales per year, is profitable and has an incredible "Apple-like" brand, offers personalized services through the combination and innovation of medicines and their powerful AI MedMatch runs in the background. Conclusion: PRIME Video didn't destroy Netflix, PRIME Music didn't destroy Spotify and similarly HIMS won't be overrun by Amazon or other competitors. HIMS has an incredible team and will execute like there is no tomorrow!

©Copyright. All rights reserved.

Wir benötigen Ihre Zustimmung zum Laden der Übersetzungen

Wir nutzen einen Drittanbieter-Service, um den Inhalt der Website zu übersetzen, der möglicherweise Daten über Ihre Aktivitäten sammelt. Bitte überprüfen Sie die Details in der Datenschutzerklärung und akzeptieren Sie den Dienst, um die Übersetzungen zu sehen.