AI and real revenue? These often don't go together. However, I'm introducing you to an AI company with a revenue growth of over 20% per year over the past five years and a revenue of $1 billion in 2024 alone.

updated: 14th of April 2025

1. Overview

ZETA operates so-called "customer lifecycle management," meaning the information and actions we share and perform digitally are analyzed by AI. Thanks to its 235+ million consumer database, companies gain valuable insights into consumer (purchasing and digital) behavior. Through their ZMP platform, campaigns reach customers via various channels such as messaging and social media.

What makes the company so exciting? ZETA is a high-growth AI stock trading at a discount. ZETA was founded in 2007 by David A. Steinberg and John Sculley (former CEO of AAPL and President of PEP).

2. Business Model

ZETA specializes in AI, data analytics, and machine learning. It offers companies the ZMP Platform (ZETA Marketing Platform) to optimize marketing campaigns based on extensive data sets. ZETA combines first-party data with proprietary AI algorithms to predict customer behavior and maximize conversion rates. By precisely personalizing customer interactions, ZETA analyzes large amounts of data to create highly accurate campaigns. What business areas does the ZETA Marketing Platform (ZMP) have?

- Data analysis and segmentation

- Personalized advertising campaigns

- Omnichannel marketing (email, social media, mobile, web)

- Marketing process automation

ZETA's Data Cloud contains billions of data points from first- and third-party data sources. Companies use these to gain better insights into customer behavior and develop more precise marketing strategies.

3. Market position

How strong is ZETA's market position?

Major players like Salesforce, Adobe, and Oracle hold strong market shares. ZETA stands out from the competition with its sophisticated AI technology and the enormous amount of actionable data it has.

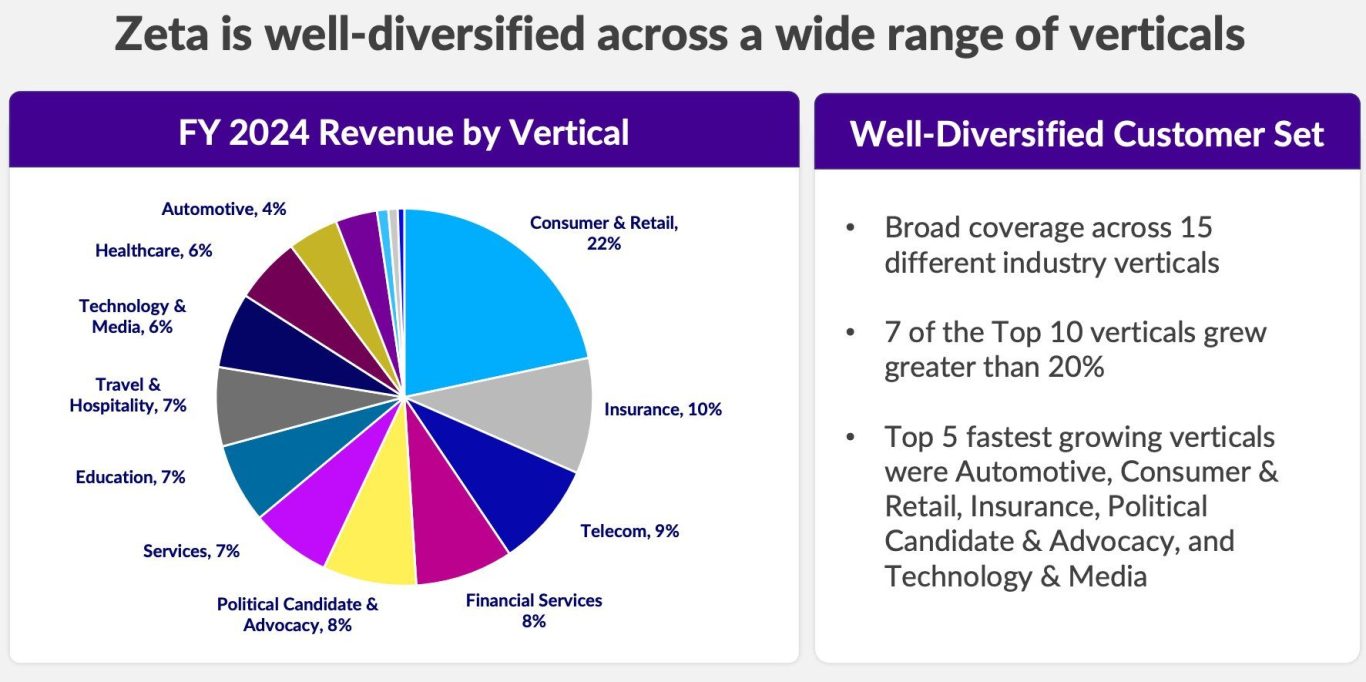

With hundreds of customers from various industries—including retail, financial services, healthcare, etc. - ZETA has established a solid market position. It serves customers in over 15 different industries.

Additionally, ZETA has 44% of the Fortune 100 as customers, another very impressive fact.

ZETA's Competitive Advantages

- AI-Powered Decision-Making

- Comprehensive Data Basis

- Automation & Personalization

- Omnichannel Approach

- Cost-Efficiency

4. How is $ZETA growing based on the Q4'24 numbers?

ZETA achieved revenue of $315 million, an increase of 50% YoY, gross margin remained stable, and profitability continues to improve.

5. ZETA Stock Valuation - EV/Sales 2025

Annual Revenue (estimated for 2025): ~$1.2 billion

Enterprise Value (EV): ~$4 billion

EV/Sales = $4 billion / $1.2 billion = ~3.3x

Interpretation: The EV/Sales multiple of 3.3x is relatively fair compared to other MarTech companies.

Comparison:

The Trade Desk (~7x) → more expensive

Salesforce (~5x) → slightly more expensive

Adobe (~6x) → more expensive

ZETA is therefore comparatively cheap.

Based on its 2025 forecasts, ZETA continues to perform strongly, significantly increasing both revenue and profitability. Furthermore, ZETA has outlined a path to 2028.

Based on a 20% compound annual growth rate (CAGR), ZETA plans to significantly increase its revenue, EBITDA and free cash flow over the next 4 years.

5. Conclusion: Is $ZETA an attractive stock for 2025?

Pros: Moat, High growth rates, Scaling & increasing profitability, EV/Sales of 3.3x is favorable compared to the competition, solid cash flow generation.

Risks: ⚡ Strong competition (Salesforce, Adobe, The Trade Desk) ⚡ Advertising market is cyclical – could suffer in a recession.

©Copyright. All rights reserved.

Wir benötigen Ihre Zustimmung zum Laden der Übersetzungen

Wir nutzen einen Drittanbieter-Service, um den Inhalt der Website zu übersetzen, der möglicherweise Daten über Ihre Aktivitäten sammelt. Bitte überprüfen Sie die Details in der Datenschutzerklärung und akzeptieren Sie den Dienst, um die Übersetzungen zu sehen.